Subdivisions typically aren’t built to earn rent. They are built to sell off lots or homes, so the income approach differs. This sheet represents the income approach for Subdivisions and is a form of DCF known as the Subdivision Development Method. The DEVMETHOD sheet will be used to model a sell-off of the lots.

This guide shows how to access and use the DEVMETHOD | Development Method sheet

Pre-Requisites

-

Subscription Tier: Professional (with the Subdivision Add-on) or Enterprise

- This is not included in the base Professional subscription and requires an add-on service. If you would like to discuss accessing the Subdivision Workbook and Report Template, please contact your Client Success Manager or Support@valcre.com to assist.

- Subdivisions must be enabled by a Valcre administrator.

- Valcre Add-In version 2.0.8.0 or higher

- Valcre Workbook version 1.4.25 or higher

- A partially started (at minimum) Job in Valcre Online

- Set up the Valuation Workbook for Subdivision work.

Table of Contents

- How-to-Guide

How-to Guide

Step 1: Access the DEVMETHOD sheet by selecting DEVMETHOD from the bottom or side navigation menu.

Step 2: Review the applicable Premises.

We have provided three different discounted cash flow analyses. One will typically be used for an As-Is value, another will typically be used for a Prospective Upon Completion value, and the last can be used to model contractual absorption or an alternative development plan.

Pro tip: Typically, you will have an as-is value. If the property is just raw land, then there will be a lot of costs involved in the as-is value, such as land planning, construction of the lots, etc. The as is value could have some lot construction costs. If you have a prospective upon completion, this assumes that the lots are already built. There wouldn’t typically be lot development costs involved.

Step 3: Enter the Effective Date for each applicable Premise.

Step 4: Indicate whether you want to Grow Income and Expenses Before the Start Date.

- As-Is: This is irrelevant because the Start and Effective dates are the same.

-

Prospective Upon Completion, everything you enter is based on current terms, but the cash flow start date will be in the future.

- For example, you have determined the lots will sell for 90K each, but you are anticipating some inflation or appreciation before they start selling off the lots. In this instance, you would select Yes to indicate this.

Step 5: Select the appropriate Discounting option.

Step 6: Select the appropriate Unit Type.

Choose what kind of unit they are selling for each premise.

Step 7: Select the appropriate Unit Source.

Determine what you want the source of the unit to be.

- IE. What are you modeling this off of? (Phase 1, phase 2, all the lots, unit count instead of lots)

Step 8: Enter the anticipated number of Units Presold.

Determine how many units are anticipated to be presold. (This would indicate the Lot Sales you don’t want to be discounted.)

Step 9: Enter the anticipated Unit Sale Price.

Step 10: Indicate the Absorption Rate.

Pro-tip: Consider using your conclusion from the CMA6 sheet.

Step 11: Indicate the compound growth rate you wish to use for the unit prices in the Unit Price Change field.

Step 12: Enter the Cost Per Unit.

Step 13: Indicate if the Lot Cost will increase and the anticipated rate for the increase using the Cost Increase field.

Step 14: Indicate if any taxes will be applied to period 0 using the RE Taxes Period 0 Field.

Step 15: Indicate the anticipated Real Estate Taxes for unfinished or raw lots using the RE Taxes Per Raw Lot field.

Step 16: Indicate the taxes per unit on built lots but unsold using the RE Taxes Per Completed Unit field.

Step 17: Indicate how fast you anticipate taxes to grow using the RE Tax Increases field.

Step 18: Enter the appropriate Marketing Fees. They will be applied as a percentage of gross sales.

Pro Tip: the Marketing Fees are fees paid to advertise that lots are for sale, not commissions. Commissions are calculated on the lot values or prices and go into closing costs.

Step 19: Indicate anticipated Closing Costs. They will be applied as a percentage of gross sales.

Step 20: If applicable, indicate if there will be Association Dues for Period 0.

Step 21: If applicable, indicate how fast you anticipate Associate Fees to grow using the Association Dues Increases field.

Step 22: Indicate all Overhead | Carrying Costs. They will be applied as a percentage of gross sales.

For example, legal, insurance, etc.

Step 23: If applicable, indicate any Entrepreneurial Incentive.

- You may opt to choose a discount rate that is inclusive of the Entrepreneurial Incentive.

Step 24: If applicable, indicate the Safe Rate. The safe rate will be applied to negative cash flows only.

Step 25: Indicate the Discount Rate. The discount rate will be applied to the positive cash flows.

AS-IS Market Value Development Method AbsorptionTable

This is the first DCF table typically used for As-Is, indicating what kind of discounting is selected.

- Period 0 will have no discounts, as evidenced by the present value factor.

- Pro-tip: You can hide any unused columns, be careful not to hide the totals column.

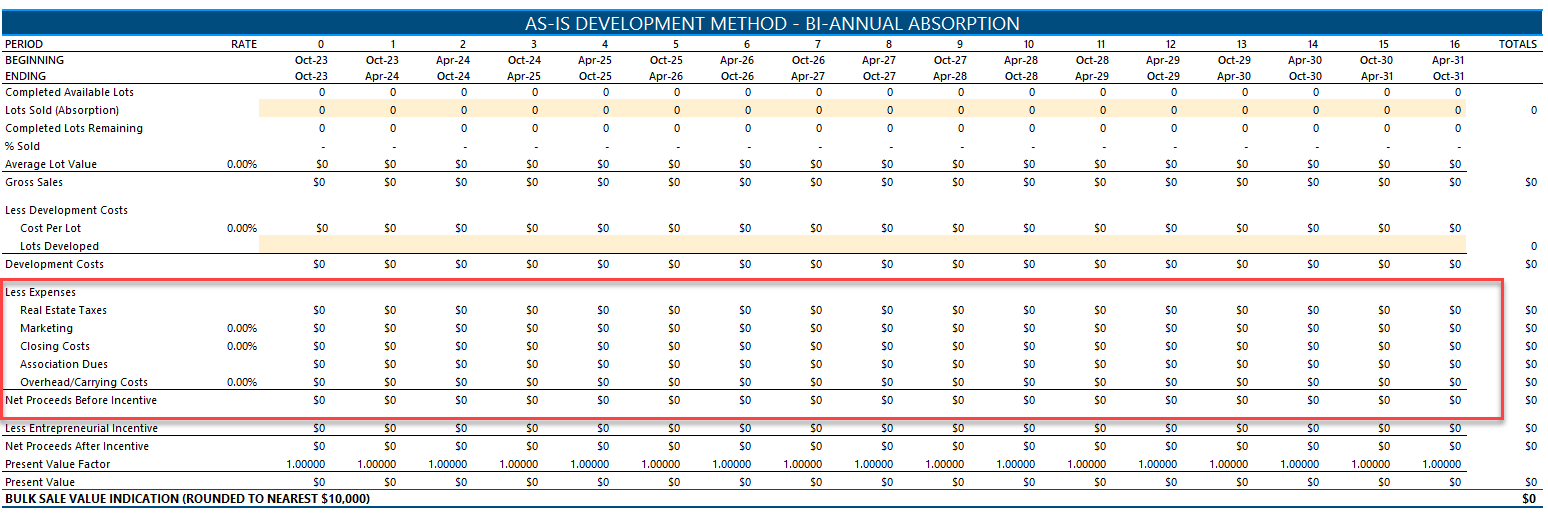

Step 1: Review the AS-IS Market Value Development Method - Bi-Annual Absorption Table

- Completed Available Lots: This indicates how many lots could be sold.

- Lots Sold

- Period 0 indicates what you think will be presold. The future is based on the absorption rate.

- Pro-tip: This will default to the absorption rate, but you can override it if you feel there will be a ramp-up or decline in sales.

- Completed Lots Remaining: indicates how many completed lots are remaining over time. This should end in 0.

- Average Lot Value: The inflation rate will apply over each period.

- Gross Sales: Multiplies the lots absorbed in that period by the average lot value

- Cost Per Lot: Lot development costs

- Lots Developed: Enter the lots as they are developed. This is a manual entry field, not automatic, as it can vary per development.

- Development costs: shows total lot development costs.

Less Expenses

- Real Estate Taxes: A separate table calculates those in a lower section on this sheet.

- Marketing: Summary of the marketing costs input in step 18. These costs are usually calculated as a percentage of gross sales.

- Closing Costs: Includes commissions, title fees, etc, and are calculated as a % of gross sales

- Association Dues: Calculated based on a separate table below the taxes table.

- Overhead and Carrying Costs: Calculated as a percentage of gross sales.

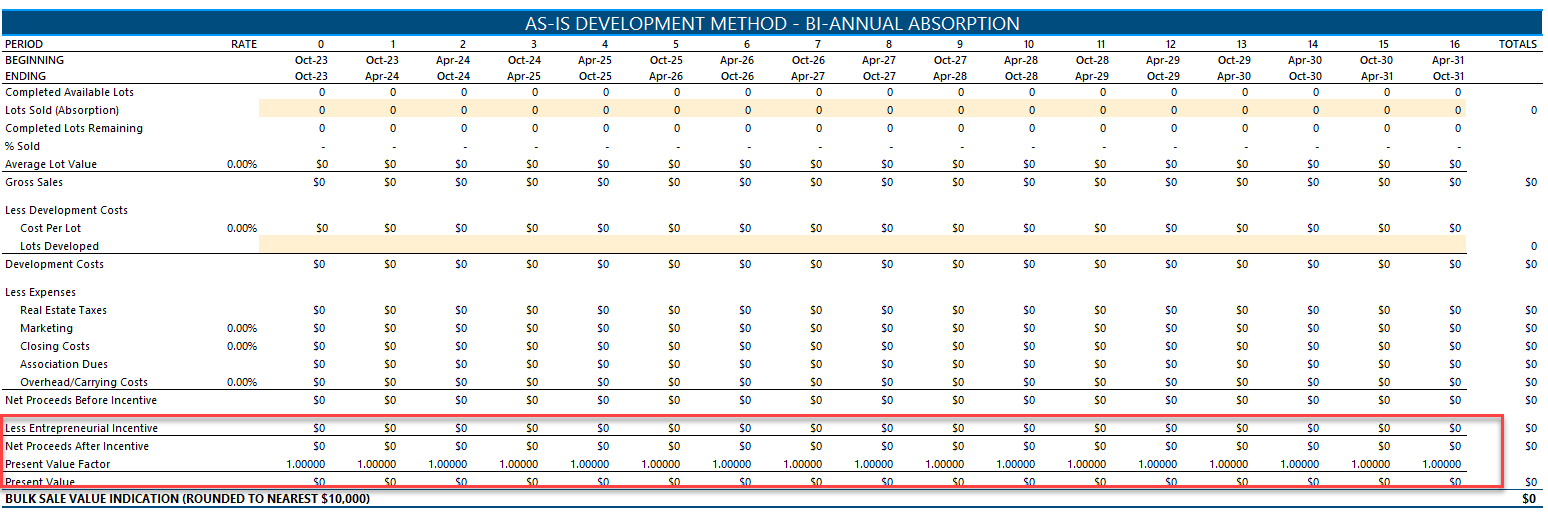

Less Entrepreneurial Incentive

- Present Value Factor: This shows the reader how it was calculated. When the net proceeds after the incentive is a negative number, it will be discounted based on the safe rate indicated above. The positive cash flows will be discounted based on the indicated discount rate above.

- Present Value: added up and rounded by selection.

Additional Metrics

These are added metrics that may or may not apply to your valuation and can be used as applicable.

- Bulk Sale Value Per Lot: This is a quick way to see the bulk value per lot

- Implied Bulk Sales Value Per Lot: Divides the Bulk Sale Value indication above by the Total Number of Lots.

- Bulk Sale Value: same as Implied Bulk Sales Value Per Lot; however, it’s the rounded number based on the indicated round to nearest in this section.

Aggregate of the Retail Values

Here is where we display the Aggregate Of The Retail Values, Inflated and Uninflated

Inflation - based on the fact they won’t all sell in period 0; by the time they sell, they will be at potentially higher values.

- Bulk Sale Value/Aggregate of Retail Value: Shows the bulk value divided by the aggregate of the retail values as a percentage for both inflated and uninflated.

- Aggregate of the Retail Values Less Bulk Sale Value: - subtracts the Bulk Sale Value from the Aggregate of the Retail Values.

-

Implied IRR before EI: if you aren’t using any EI, the Implied IRR assumes they are buying it at the price that you say the value is and uses the actual cash flows before incentive because it’s an internal rate of return, not external.

- It does not consider the profit.

- If you aren’t including EI, it will be very close to the determined discount rate. The difference is rounding and/or using the Safe Rate for negative cash flow.

- If you use a separate line item for profit, the Implied IRR will be much higher than the discount rate entered at the top of the sheet. Because one considers you are taking out money for EI. It’s a cross-check to see if your Implied IRR is reasonable if you use a line item for profit.

AS-IS Development Method Taxes Table

The table considers that if lots are sold on average in the middle of each period, no taxes will be due for the last half of the period. These numbers feed into the cash flows indicated above.

Repeat these steps for the other premises.

Association Dues Table

Association dues may not always be applicable but could be applicable if the subject is part of a master-planned community or a later phase of an existing subdivision. Association dues may be required to be paid after lots are completed.

Once you have completed this sheet, you can begin work in the LOTVALUES sheet.

For additional questions about using the DEVMETHOD sheet, please contact Valcre Support using the live chat feature in Valcre Online or Valcre Mobile.

Comments

0 comments